We often hear that “Money can’t buy happiness,” and while it’s true that money can’t buy happiness, money can buy things that contribute mightily to happiness.

For one thing, money gives us freedom from worrying about money, which is certainly one of the greatest luxuries that money can buy.

We can use money to put our values out in the world—by giving to causes we believe in, and supporting our communities and the people we love.

We can buy experiences, because sometimes when we’re buying a thing, we’re also buying an experience: a bicycle, a camera, a plane ticket.

We can buy possessions that make our lives easier, richer, healthier, and that allow us to project our identity into our surroundings.

Money is tool. It can be used to support our happiness, or not, depending on our choices.

For aims relating to Mindful Investment—how we mindfully spend our time, money, and energy—it can be difficult to know where to start, and how to distill aims into concrete steps.

For the “money” part of the Mindful Investment equation, I wanted to talk to a finance expert, so I got in touch with my longtime friend Ramit Sethi.

Ramit Sethi is a personal finance adviser, author of the New York Times bestseller I Will Teach You to Be Rich, and founder of GrowthLab and I Will Teach You To Be Rich.

I don’t even remember how Ramit and I first met. We’re interested in many of the same subjects; at some point, our paths crossed.

I was so happy for him when he recently hosted his own Nextflix series: How to Get Rich. Thrilling! Here’s the show: “Money holds power over us—but it doesn’t have to. Finance expert Ramit Sethi works with people across the U.S. to help them achieve their richest lives.”

One thing I admire about Ramit’s approach is that he’s very concrete, and he has a strong point of view. I couldn’t wait to talk to him about using money as a tool to help us make our lives happier, healthier, more productive, and more creative.

He had many ideas about specific, practical steps for people working toward Mindful Investment aims.

Gretchen: You talk a lot about cultivating a “rich life”—what is a “rich life?” How does it go beyond money and possessions?

Ramit: Your Rich Life might be traveling for 3 months per year. Or buying a beautiful cashmere coat. Or it might be picking up your children from school every afternoon.

Your Rich Life is yours! And yours will look very different from mine. That’s the beauty of designing your Rich Life like a painting—it will be personal and fit you like a glove.

At this point in my life, my Rich Life is traveling for 2-3 months per year, working with people I like and respect, and spending extravagantly on beautiful hotels and convenience while cutting costs on things like my 18-year-old car that I still drive.

Of the 10 categories of habit loopholes I’ve identified, which ones do you see people employing most often, in an unhelpful way, when it comes to their finances?

False choice loophole—or, “I can’t do this, because I’m so busy doing that.” With money, we say: “I don’t want to have to track how much I spend on carrots for the rest of my life” (you don’t).

Tomorrow loophole—or, “It’s okay to skip today, because I’m going to do this tomorrow.” With money, we say: “I’ll start investing later” and “My Rich Life is traveling once I retire” (even though we would never say “I’ll wait until I retire to start making friends”).

Lack of control loophole—or, “I can’t help myself.” With money, we say: “I’m not good at investing” (even though money is a skill we can learn).

You emphasize the value of automating finances. In the context of spending with purpose, is there room for spontaneity?

Automation gives us room to be spontaneous! For example, if I’ve set aside money for a vacation, I’ve added an extra 15% to account for unexpected things that come up. When I sit down for dinner, I’m not thinking about how much an extra appetizer costs—that’s already been saved for months before! If we decide to take a spontaneous food tour or even extend our trip, automation allows that to happen.

You talk a lot about setting up simple money systems and routines. What are some regular habits, practices, or “money rituals” you’ve heard of people using that reinforce mindful, intentional investing and spending?

- They talk about money regularly, positively, and proactively. Most people only talk about money when they fight about it—or something goes wrong. If you feel bad about money, why would you ever want to engage with it? But if you set up a regular time to talk about money—I recommend once per month, with a pre-set agenda, and always starting with a compliment for the other person about how they handle money—you’ll make money a regular part of your life.

- They create Money Rules. Here are my personal money rules. These are just for me! They might not make sense for you. But people who are savvy with food or clothes or travel create their own back-of-the-napkin rules. We should do the same for money.

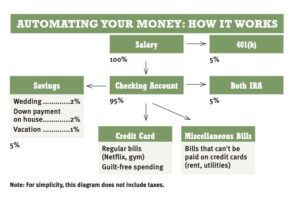

- They automate money. I spend less than 1 hour per month on my finances—and you should too! Here’s my money automation system:

For people feeling overwhelmed by their finances, what’s one small, concrete step they could take today to address their situation?

There are 4 key numbers that really matter in your finances. You can come up with these in about 15 minutes and get 85% accuracy. Here they are:

- Fixed costs (should be 50-60% of your take-home pay). Includes mortgage/rent, car payments, debt payments, groceries, subscriptions, childcare—any expenses that are fixed, or required, each month.

- Savings (5-10%). The money you save for an emergency fund, vacation, etc. This is money you typically don’t need for 1-5 years.

- Investments (5-10%, the higher the better). This is where real wealth is created. All investments count towards this number.

- Guilt-free spending (20%-35%). This is my favorite category. It can be clothes, travel, eating out…whatever you want!

By looking at your finances with this bird’s-eye view, you can see how you stack up. And then you can start to be intentional about where your money goes. You can use this template to make your tracking easier.

How might you approach spending, saving, and investing money in a way to achieve your aims for yourself? It’s an important question.